Why can't these advisors get paid?

When an unusual recruiting deal between Credit Suisse and Wells Fargo went awry, years of broker frustration, severe attrition and litigation followed. Also at stake: Up to $245 million in back pay.

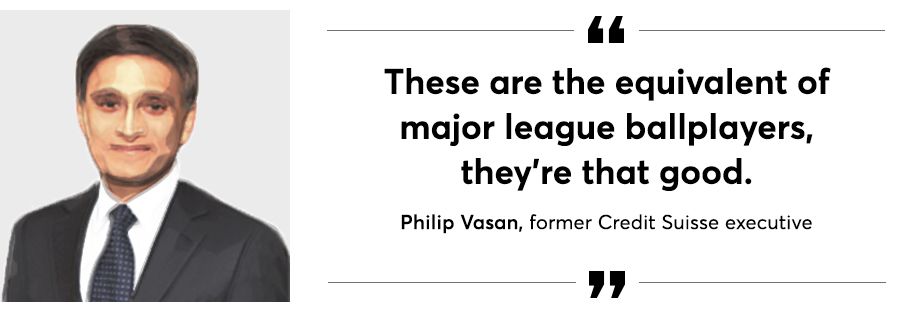

There was $93 billion in client assets on the line. The advisors managing that fortune were “the equivalent of major league ballplayers.” And Wells Fargo had a unique opportunity to hire all 292 of them in one shot.

The pitch had to be perfect.

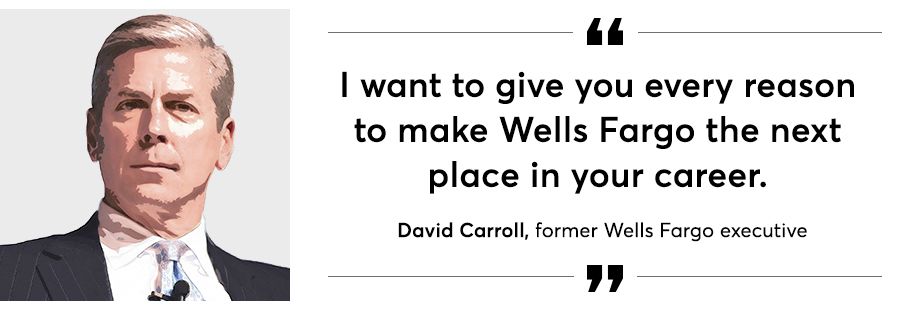

"I am here unabashedly to sell you on Wells Fargo, 'cause we're very proud of this business,” is how David Carroll began his appeal to this group of Credit Suisse advisors.

Wells Fargo would “pull out all the stops,” Carroll, then head of wealth and investment management at the firm, said during an October 2015 virtual town hall meeting.

Carroll had ample reason to sell them on Wells Fargo. As a former Credit Suisse executive later said in arbitration testimony, these advisors were “world class.” They oversaw more than $93 billion and generated more than $426 million in revenue.

Carroll’s pitch came after Wells Fargo had entered into an unusual deal with Credit Suisse. The Swiss bank wanted out of its U.S. private banking unit, but couldn’t find a buyer. Rather than sell the business, Credit Suisse gave Wells Fargo exclusive rights to hire its brokerage force. In other words, instead of buying the New York Yankees, Wells Fargo would hire each individual player.

Yet the unusual recruiting arrangement planted seeds for broker frustration, severe attrition, a regulator’s admonition and years of litigation and recriminations over whether Credit Suisse had wrongfully withheld up to $245 million in back pay from employees — or whether its former employees were just greedy double dippers "who hit the lottery" and were claiming to be "victims,” as a company spokeswoman put it in a statement.

For the advisors, “You can’t underestimate the personal feelings of betrayal up and down the line,” says Danny Sarch, a recruiter who helped some Credit Suisse brokers find new employers.

'I think we have our horse'

By late 2015, Credit Suisse advisors Joe Lerner and Anna Winderbaum, were facing a professionally challenging situation: The firm they’d been with the entirety of their advisory careers was in upheaval and they needed to find a safe harbor for themselves and their clients.

Lerner and Winderbaum, who operated as a team, had been through disruptive change before. Both started their careers in the late 1990s at Donaldson, Lufkin & Jenrette, and they stuck with the company following its acquisition in 2000 by Credit Suisse.

During their time at the firm, Lerner and Winderbaum built up a substantial practice catering to wealthy clients. They each earned over $1 million per year. They joined the bank’s exclusive chairman’s club for top advisors. By 2015, Lerner and Winderbaum oversaw more than $1 billion in client assets, according to documents filed in a New York State court by Credit Suisse.

But changes were afoot. In March of that year, Credit Suisse named a new CEO: Tidjane Thiam, a former McKinsey consultant and insurance executive. Thiam initiated a review of the bank’s operations with an eye to cutting costs and reorienting its strategic focus to areas with higher growth potential.

By that August, Lerner, Winderbaum and other advisors learned the strategic review had the U.S. wealth management business in its sights. The unit was deemed “subscale with severely challenged profitability,” according to an executive summary of the review, dubbed Project Light.

This and other internal company documents, as well as emails and legal memos referenced in this article, were filed in New York State Supreme Court this year as part of ongoing litigation between the bank and these two advisors.

Offloading the U.S. wealth management unit would release capital for other uses and relieve Credit Suisse of this burden, the executive summary said. However, there were a limited number of potential buyers due to U.S. platform and licensing requirements. Plus, advisors’ wealthy clients had highly sophisticated investing needs that limited the range of firms that could accommodate the business.

The bank began to shop the unit around.

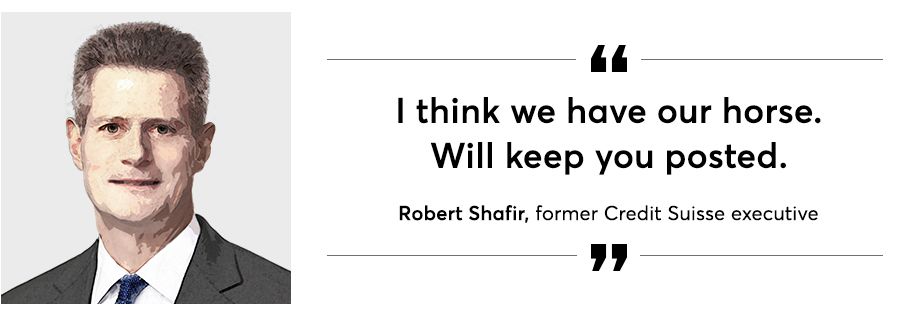

Discussions with Morgan Stanley that summer went nowhere, while interest from Wells Fargo increased. A September meeting between Credit Suisse and Wells Fargo “went very well,” Robert Shafir, Credit Suisse CEO for the Americas region, told Thiam in a Sept. 10 email. “I think we have our horse. Will keep you posted.”

On Oct. 20, Credit Suisse told employees it was exiting the U.S. wealth management business and giving Wells Fargo exclusive recruiting rights to its advisors.

How the firm designed and executed its exit strategy proved to be highly contentious, especially around a simple question: Were the advisors laid off, or did they resign voluntarily? Millions of dollars in legal claims hinge on the answer.

“It comes down to corporate greed. … They’ve spent all this time avoiding paying that [deferred compensation] liability. It’s been carefully structured to avoid doing just that,” says Barry Lax, an attorney at law firm Lax & Neville, which represents 30 advisors, including Lerner and Winderbaum, in litigation with Credit Suisse.

'You're making a huge-ass mistake'

When Credit Suisse told employees it would exit the U.S. wealth management business, Lerner, Winderbaum and nearly 300 other advisors had pressing questions: Where would they work now? How long did they have to make a decision on whether to go with Wells Fargo? What would happen to the deferred compensation Credit Suisse owed them?

Credit Suisse management told advisors that October that they had until Dec. 7 to decide whether to take the Wells Fargo offer to join the firm. During the October town hall, Wells Fargo executives touted the firm’s platform, capabilities and brand.

The bank also dangled a signing bonus equal of up to 300% of an advisor’s revenue, to be paid in a combination of upfront cash and deferred compensation. Wells Fargo executives also invited Credit Suisse advisors to visit their brokerage offices in St. Louis.

“We want to give you an opportunity to see us from the inside. And you be the judge as to whether or not this is a good fit for you,” Carroll said.

Even before advisors had their plane tickets in hand, tensions emerged. During the townhall’s Q&A, executives assured skeptical Credit Suisse brokers that Wells Fargo’s low recognition in the ultrahigh-net-worth client segment wasn’t a problem. “I would tell you that the fact that you don’t run into us is a strength,” Carroll said.

One Credit Suisse advisor asked if Wells Fargo would bring over the product, middle office and support staff, as well. If not, “you’re making a huge-ass mistake,” the advisor said. Carroll replied no, Wells Fargo had its own staff.

Still, Lerner, Winderbaum and many of their colleagues made the trip to St. Louis — only to find Wells Fargo to be an ill fit. They discovered that Credit Suisse was retaining some of their clients’ business even as it was offloading the advisors. When Lerner and Winderbaum spoke with Mary Mack, head of Wells Fargo Advisors, in St. Louis, they say she told them that that the firm couldn’t accept a loan belonging to their largest client, pursuant to its deal with Credit Suisse. “As this single loan accounted for almost half of [Lerner and Winderbaum’s] production, they knew immediately that Wells Fargo’s offer was a nonstarter,” the advisors’ arbitration filings say.

Wells Fargo declined to comment for this article. Carroll, Lerner and Winderbaum also declined to comment.

There also was bad news on deferred compensation: No one would get any. Instead, advisors transitioning to Wells Fargo would resign from Credit Suisse, get hired by the wirehouse and receive “what we think is going to be a very compelling onboarding award” in cash, said Philip Vasan, who then served as head of the private bank for Credit Suisse in the Americas.

“And if you do not go to Wells Fargo, that's not available to you. It's exclusive in complete alignment with our [advisors] who stay with the program and go to Wells Fargo. Anything else is a voluntary resignation to a third party,” Vasan said during the October town hall.

Reached for comment, Vasan, who now works at BlackRock, referred questions about the deferred comp issue to Credit Suisse.

Game-changing opportunity

Pitch made. Invitations sent. Offers tendered. What followed the Wells Fargo-Credit Suisse announcement was a recruiting bonanza — for rival firms.

UBS, Morgan Stanley and other brokerages dangled enormous hiring bonuses to snatch away the best talent. In Lerner and Winderbaum’s case, it totaled $25 million, according to Credit Suisse. For some advisors, signing bonuses comprised of upfront and deferred compensation approached nearly 400% of their annual revenue. Competitors were outbidding Wells Fargo and offering what some advisors deemed better working conditions.

In a summer 2015 internal report, Credit Suisse managers estimated that advisor attrition in the event of a sale could run as high as 22%. In the end, it was much worse than expected: Wells Fargo retained about one-third of Credit Suisse’s 292 advisors.

Morgan Stanley leadership was eager to sign Lerner and Winderbaum, even as the firm struggled to accommodate other Credit Suisse advisors seeking refuge. Managing Director David Jarach emailed Vincent Lumia, head of private wealth management, on Sept. 18 to say he was working on giving Lerner and Winderbaum “the full tour,” but schedules were tight.

“It has been tough to find a date because there are so many CS teams coming in that the VIP resources are stretched thin,” Jarach wrote.

“Great, game changing oppty [sic],” Lumia replied.

On Nov. 14, Wells Fargo extended them an offer of employment and a signing bonus of six payments totaling approximately $8.7 million. It wasn’t clear from court records how much of an onboarding award Credit Suisse offered to entice Lerner and Winderbaum to “stay with the program,” as Vasan had put it in the town hall.

Around the same time, Morgan Stanley offered the team a nine-year deal totaling $25 million, according to court documents filed by Credit Suisse.

Lerner and Winderbaum went to Morgan Stanley.

When the duo parted ways with Credit Suisse on Dec. 11, the firm owed them $1.8 million in deferred compensation, the advisors say.

‘Forced into this position’

When Lerner and Winderbaum handed in their resignations, they pinned the cause on Credit Suisse’s decision to exit the business. “I am not voluntarily resigning but have been forced into this position,” the advisors wrote.

Credit Suisse sees the matter differently. It claimed in a May 2019 court filing that it “did not take any steps to sever its employment relationship" with Lerner and Winderbaum.

It may seem like semantics, but the words are of enormous importance. How advisors part ways with their employers has bearing on legal claims for deferred compensation. Under Credit Suisse employment agreements, advisors lose their deferred compensation under certain circumstances, such as a voluntary resignation or termination with cause. An involuntary termination, however, could theoretically result in back pay being owed.

“If it had been an acquisition,” Vasan later testified in arbitration, “then everyone would have simply changed what legal entity they were in on a certain date. But because this was a hiring arrangement, it was structured such that the relationship managers [the financial advisors] would voluntarily resign, but specifically to go to Wells Fargo, as opposed to go to some other place.”

From the point of view of the advisors who are suing, Credit Suisse forced advisors’ hands, masking a layoff as a voluntary resignation. And, they claim, the firm has so far avoided paying millions in deferred compensation through obfuscation and delaying tactics.

Credit Suisse allegedly kept advisors in the dark as to key details of when it would shutter its U.S. wealth management unit. It wasn’t until February 2016 that the firm informed the remaining few advisors that their final day would be soon after: March 31. Regardless, staying to the end wasn’t feasible as client portfolios required tending.

“The branches were shutting down, advisors and support staff were leaving en masse, and Credit Suisse was selling off furniture and equipment,” Lerner and Winderbaum say in legal filings.

The firm allegedly attempted to stifle advisors’ deferred comp claims by forcing legal complaints into arbitration forums run by a private mediation company paid by Credit Suisse. Ex-employees say this gave the firm an unfair advantage.

After advisors’ attorneys complained to FINRA, the regulator publicly reasserted advisors' right to take employment disputes to its arbitration forums. Dozens of FINRA arbitration claims have since been filed, and arbitrators have recently started issuing rulings. The firm persuaded a judge to nix a lawsuit seeking class-action status that was brought by an advisor who'd moved to UBS. The bank settled some cases for undisclosed amounts while other advisors have withdrawn their claims, according to people familiar with the matter. In five cases, FINRA arbitrators have awarded advisors more than $11 million in damages.

Lerner and Winderbaum won $6.7 million earlier this year when a panel of three FINRA arbitrators sided with them against Credit Suisse. The arbitrators also ruled that a regulatory record known as a U-5 should have their reason for termination changed to “other” and the explanation to “terminated without cause,” which is vital for advisors who hope to be hired by new firms.

Credit Suisse hasn’t given up its fight, insisting the arbitrators got it wrong. The firm recently asked a state court to vacate the decision.

Lerner and Winderbaum were exempt from New York State labor law, which did not cover certain categories of employees, such as executives and managers, the bank asserted. As evidence, the firm notes that the advisors had been mentoring younger employees and serving on corporate committees. Plus, Lerner and Winderbaum’s pay did not constitute wages under the law, Credit Suisse said in arbitration proceedings.

Credit Suisse claims advisors who moved to other firms and are now seeking their deferred compensation are double dipping. These advisors got lucrative signing bonuses because they used their outstanding deferred comp as a negotiating ploy to boost the size of the deals. In essence, advisors got a “make-whole,” Credit Suisse claimed in legal documents.

“This was not the end of the world for them,” the company’s attorney said in closing arguments during the Lerner and Winderbaum arbitration. “In fact, it was the chance of a lifetime, because they were able to monetize their book of business.”

The advisors' attorneys reject this argument.

“The wage laws in all the states I deal with do not say, ‘People who make more than $1 million aren’t covered by this.’ The wage laws are designed to protect everyone equally,” says Brian Neville, also a partner at the Lax & Neville law firm.

Morgan Stanley, UBS or any other firm that hired a Credit Suisse advisor did not therefore accept taking on Credit Suisse’s liabilities, Neville and Lax say. And the attorneys note that among the arbitrators who ruled in favor of Lerner and Winderbaum was a professor of labor law.

Credit Suisse’s request to vacate the $6.7 million award is currently before New York State Supreme Court Judge Andrea Masley. But even if Masley rejects Credit Suisse’s petition, Lerner and Winderbaum’s prolonged battle might not be over.

In a similar case, former Credit Suisse advisor Nicholas Finn won nearly $1 million in damages against the firm in November 2018. Credit Suisse subsequently asked a state judge to vacate the award. The judge ruled in favor of the advisor. Credit Suisse is appealing that decision.

“Credit Suisse is fully committed to vigorously defending against each and every case that seeks unjust double compensation,” a company spokeswoman said in a statement. “In most of these cases, the claimants are improperly attempting to be paid the same dollar twice. Credit Suisse was fully transparent with brokers and informed them in the fall of 2015 that the transition process would run through the first quarter of 2016, giving them five months to choose to move to Wells Fargo or use that offer to negotiate with any other firm.”

Other arbitration cases involving advisors' deferred comp claims are reaching their conclusion. Lax & Neville represent about 30 former Credit Suisse advisors seeking compensation from their ex-employer. For Lerner and Winderbaum, their case is pending. It’s been three years and 10 months since their last day at Credit Suisse.

Like what you see? Make sure you're getting it all