-

New financial assessment requirements may make reverse mortgages into a retirement income tool for seniors with significant cash flow and assets.

July 29

July 29

-

Why working clients are advised to avoid borrowing from their 401(k) plans to fund their summer vacations; Plus, how Americans left $24 billion in retirement money on the table last year and the seven best places for your clients to retire overseas.

July 29 -

While the 4% rule was created to set a minimum income floor, that doesn't mean spending can never be raised. Here's a better approach to withdrawal rates.

July 28

July 28 -

Sometimes it makes sense for clients to collect Social Security before full retirement age, even if it temporarily reduces benefits.

July 28

-

Waiting for Social Security until age 70 can provide the surviving spouse with plumper payments.

July 27

-

Why timing is important for clients filing for Social Security; Plus, how to decide whether your client should invest in a 401(k) or a Roth IRA.

July 27 -

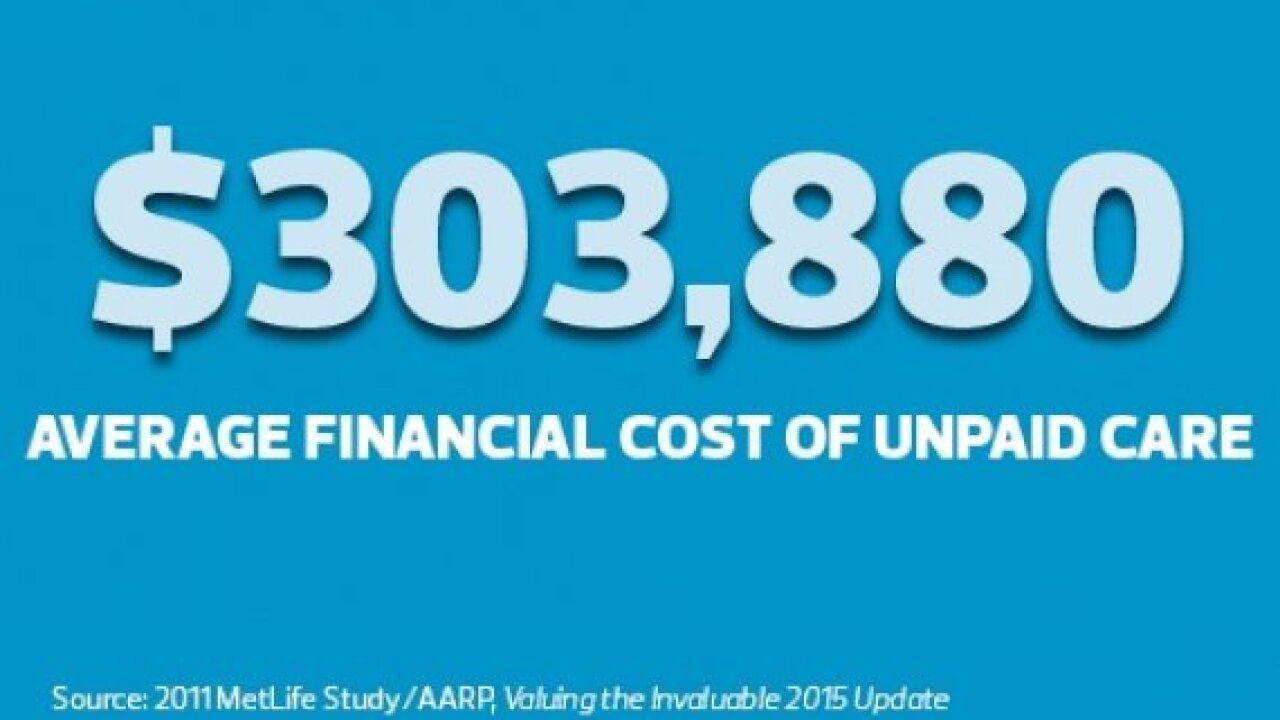

There's no doubt that professional long-term care is expensive and getting more so, but relying on family to provide care can still cost clients a fortune.

July 27

-

While raising the tax rate could help address Social Security's funding imbalance, there are other ways to shore up the program; Plus, when $1.5 million isn't enough to retire.

July 27 -

Planners should dispel these common misconceptions so that clients can make better-informed decisions.

July 24

-

Advisors and clients may not be as familiar with these other Social Security programs. Here's a brief primer.

July 24

July 24

-

Though the time period to make changes has narrowed in some instances, there are situations where Social Security allows a redo.

July 23

-

Critics charge that the fiduciary proposal will be a death knell for the brokerage model in the retirement space, leaving low- and middle-income investors without advice.

July 22 -

Potential regulatory legislation may soon restrict strategies surrounding the backdoor Roth IRA; plus, how to retire on $25,600 a year and why most clients cant even guess what their Social Security benefits will be.

July 22 -

For married couples deciding when to claim Social Security, "it's all about the survivor benefits," for the higher-earning spouse.

July 22

-

Clients can have their cake (maximum payouts) and icing (years of spousal benefits) too.

July 21

-

For some seniors, reducing adjusted gross income generates an extra tax break.

July 20

-

Women over the age of 65 are twice as likely as men to live in poverty in retirement because of lower wages, more time spent out of the workforce and lack of access to retirement savings plans.

July 20 -

Ways your elderly clients can avoid becoming the victim of a scam; plus, what you need to know about Social Security benefits and what to do if your clients' 401(k) stinks.

July 20 -

If a client old enough to receive Social Security benefits has dependent children, it could affect the calculus as to when the parent should start collecting benefits

July 19

-

Clients who keep working will see healthy gains in Social Security benefits and other financial perks.

July 17